The Buzz on Kam Financial & Realty, Inc.

The Buzz on Kam Financial & Realty, Inc.

Blog Article

What Does Kam Financial & Realty, Inc. Do?

Table of ContentsNot known Facts About Kam Financial & Realty, Inc.The Single Strategy To Use For Kam Financial & Realty, Inc.10 Easy Facts About Kam Financial & Realty, Inc. ExplainedHow Kam Financial & Realty, Inc. can Save You Time, Stress, and Money.Getting My Kam Financial & Realty, Inc. To WorkMore About Kam Financial & Realty, Inc.

We may receive a fee if you click a lender or send a form on our website. This fee in no other way impacts the details or guidance we provide. We maintain content freedom to guarantee that the recommendations and insights we supply are unbiased and objective. The loan providers whose rates and various other terms show up on this chart are ICBs advertising companions they supply their rate information to our information partner RateUpdatecom Unless adjusted by the customer marketers are sorted by APR lowest to highest possible For any type of advertising companions that do not supply their rate they are listed in promotion screen units at the base of the chart Advertising companions may not pay to boost the frequency priority or importance of their display The rate of interest interest rate and other terms advertised right here are estimates supplied by those advertising companions based on the info you went into over and do not bind any kind of lender Month-to-month repayment quantities stated do not consist of quantities for taxes and insurance policy premiums The real payment responsibility will certainly be greater if tax obligations and insurance are included Although our information companion RateUpdatecom gathers the details from the financial organizations themselves the accuracy of the data can not be ensured Prices may alter without notification and can change intraday A few of the info contained in the rate tables consisting of yet not limited to special advertising and marketing notes is provided directly by the loan providers Please validate the prices and offers before looking for a lending with the monetary establishment themselves No price is binding until locked by a loan provider.

Not known Details About Kam Financial & Realty, Inc.

The amount of equity you can access with a reverse mortgage is identified by the age of the youngest customer, present rate of interest, and the value of the home in concern. Please note that you may need to set aside additional funds from the lending proceeds to pay for taxes and insurance.

Rates of interest might vary and the stated price might transform or otherwise be offered at the time of car loan commitment. * The funds readily available to the consumer might be restricted for the first twelve month after finance closing, as a result of HECM reverse home loan requirements ((http://tupalo.com/en/users/7908107). Additionally, the debtor might require to allot added funds from the loan continues to spend for tax obligations and insurance coverage

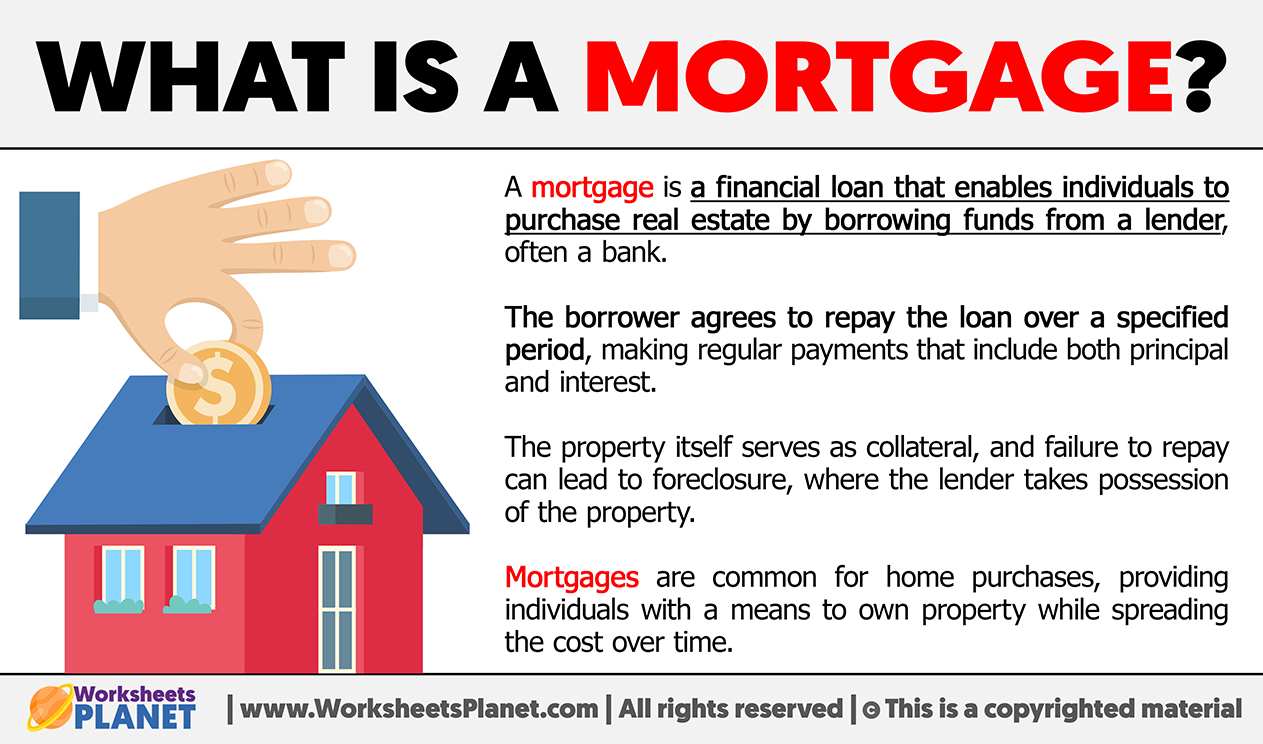

A home mortgage is essentially an economic agreement that enables a debtor to acquire a residential property by receiving funds from a loan provider, such as a financial institution or economic establishment. In return, the loan provider positions a property lien on the home as protection for the finance. The home loan purchase typically involves two major papers: a cosigned promissory note and an act of trust fund.

Some Ideas on Kam Financial & Realty, Inc. You Should Know

A lien is a lawful claim or interest that a lending institution carries a customer's residential or commercial property as security for a financial debt. In the context of a home mortgage, the lien created by the act of depend on allows the lending institution Your Domain Name to take ownership of the home and sell it if the debtor defaults on the lending.

Listed below, we will certainly look at several of the common kinds of mortgages. These home mortgages feature a fixed rate of interest and monthly settlement amount, using security and predictability for the consumer. John chooses to buy a home that sets you back $300,000 (mortgage loan officer california). He protects a 30-year fixed-rate home mortgage with a 4% interest price.

The Main Principles Of Kam Financial & Realty, Inc.

This suggests that for the whole three decades, John will certainly make the exact same regular monthly settlement, which supplies him predictability and security in his monetary planning. These home loans start with a fixed interest price and settlement quantity for a first duration, after which the rate of interest and payments may be regularly adjusted based on market conditions.

The Only Guide to Kam Financial & Realty, Inc.

These home loans have a fixed rate of interest rate and repayment quantity for the funding's period but call for the borrower to pay off the lending equilibrium after a specific period, as figured out by the lender. mortgage loan officer california. For instance, Tom wants purchasing a $200,000 residential property. (https://www.40billion.com/profile/114974493). He opts for a 7-year balloon mortgage with a 3.75% fixed rate of interest

For the whole 7-year term, Tom's regular monthly repayments will be based upon this set rates of interest. After 7 years, the remaining loan equilibrium will certainly become due. Then, Tom has to either settle the exceptional balance in a swelling sum, refinance the financing, or offer the home to cover the balloon payment.

Falsely asserting self-employment or an elevated placement within a firm to misstate earnings for mortgage purposes.

The 4-Minute Rule for Kam Financial & Realty, Inc.

Report this page